Wells Fargo & Company (WFC) is a major player in the U.S. banking industry, offering a diverse range of financial services to individuals and businesses. This includes everything from everyday banking like checking and savings accounts to more complex offerings like mortgages, loans, investment products, and wealth management services.

Key Strengths

- Diversified Revenue Streams: WFC operates across multiple business segments, reducing reliance on any single area. This diversification helps mitigate risks and provides a more stable revenue base.

- Strong Capital Position: The company maintains a solid capital base, providing a cushion against potential losses and supporting future growth.

- Improving Efficiency: WFC has been actively streamlining operations, reducing costs, and enhancing its digital capabilities to improve efficiency and better serve its customers.

Key Challenges

- Regulatory Scrutiny: WFC has faced significant regulatory challenges in recent years, impacting its growth and profitability.

- Economic Headwinds: A potential economic downturn could negatively impact loan demand, increase credit losses, and adversely affect the bank’s financial performance.

- Competitive Landscape: The banking industry is highly competitive, with numerous players vying for market share.

Recent Financial Performance (Data as of September 30, 2024 – Q3 2024)

- Revenue: $20.48 billion

- Net Income: $4.85 billion

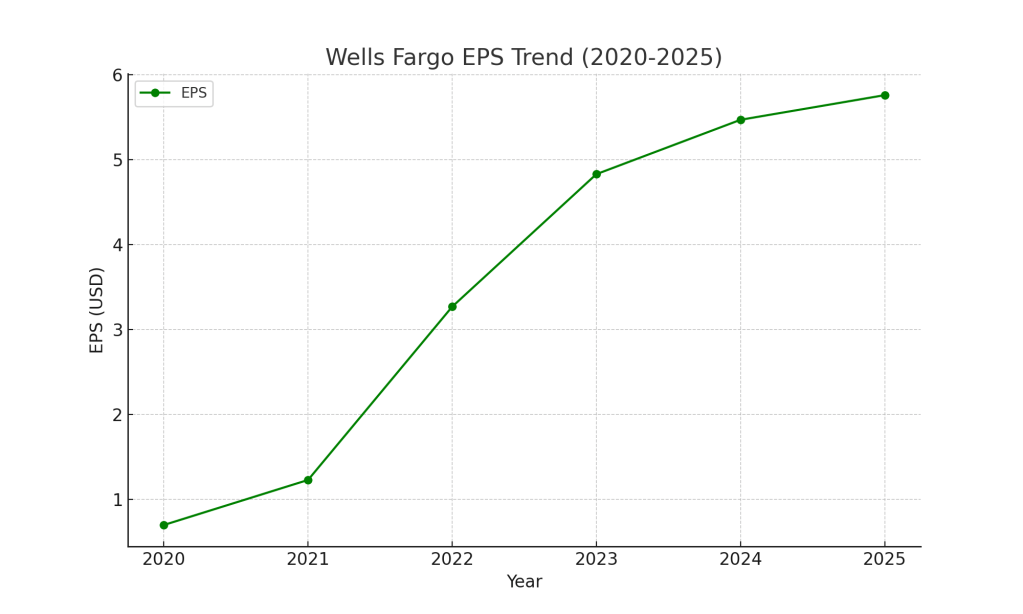

- Earnings Per Share (EPS): $1.42

- Return on Equity (ROE): 10.30% (Trailing Twelve Months)

- Return on Assets (ROA): 1.00% (Trailing Twelve Months)

- Net Interest Income: $11.69 billion (down 11% year-over-year)

- Net Interest Margin: 2.67%

- Total Loans: $910 billion

- Total Deposits: $1.36 trillion

Key Financial Trends

- Net Interest Income (NII): NII has been impacted by rising interest rates, leading to higher funding costs. The bank has been actively managing its interest rate risk, but NII remains a key area of focus.

- Credit Quality: Credit quality has generally remained stable, although there are concerns about potential deterioration in certain areas, such as commercial real estate.

- Efficiency: The bank has been making progress on improving efficiency through cost-cutting measures and digital initiatives.

Highlights

- Revenue forecast is $82.6B in 2024: In line with the $82.6B recorded in 2023. We expect the relatively weak performance to be driven by low-single-digit loan contraction and rising funding costs due to noninterest-bearing deposits flowing into interest-bearing accounts. Still, signs of a rebound are showing up in mortgage banking income and we expect investment banking income to surge past 2021’s elevated levels as WFC takes market share and benefits from strong debt underwriting.

- In Q3 2024, net interest income fell 11% Y/Y: As rising deposit costs led to 36 bps of net interest margin compression. Balance sheet movement was relatively weak as stable deposit balances were met with a 3% drop in loans. Looking forward, we expect loan momentum to return as results are positively impacted by loosening monetary policy, while deposits should rise modestly, in our view.

- As of September 30, 2024, WFC was well capitalized: With a CET1 ratio of 11.3%, well above its regulatory minimum 9.8%. Given this, we expect WFC to lean on share repurchases and repurchase approximately $19B in 2024 vs. $12B in 2023. We note WFC has cut its shares outstanding by 22% over the past five years.

Investment Rationale/Risk

- Our Buy recommendation reflects a positive view of CEO Charles Scharf: And his efforts to resolve regulatory issues. We believe WFC is in the final stages of its $1.95T asset cap (which has been in place since 2018). We also think the release of the asset cap (hopefully in 2025) will result in reputational improvement and an uptick in both loan and deposit growth. Additionally, we have been impressed with efficiency improvements as the bank has cut its physical footprint and prioritized digital (headcount down 20% over the past four years).

- This positive view is partly offset by WFC’s above-peer-average exposure to the struggling commercial real estate office sector. Still, we commend WFC’s effort to reduce risk as the bank’s Q3 2024 commercial real estate office exposure of $29.0B is down 10% from a year ago.

- Risks are a U.S. recession, weaker consumer or commercial loans, steeper credit losses, negative regulatory rulings, rising deposit competition, and failure to execute cost saves.

Business Summary

- CORPORATE OVERVIEW. Wells Fargo & Co. (WFC) is a diversified financial services company with operations around the world. WFC offers investment and mortgage products and services, as well as consumer and commercial finance, through four reportable operating segments: Consumer Banking and Lending, Commercial Banking, Corporate and Investment Banking, 1 and Wealth and Investment Management. Wells Fargo ranked 2 No. 47 on Fortune’s 2023 rankings of America’s largest corporations. In an effort to improve the bank’s efficiency, WFC has cut its headcount to 220,000 employees in Q3 2024 from over 270,000 in 2020.

- LEGAL/REGULATORY ISSUES. Corporate governance and bank practices have put the company in the spotlight for many years. Various federal and state statutory provisions and regulations limit the amount of dividends that WFC’s subsidiary banks and certain other subsidiaries may pay without regulatory approval. Federal banking regulators have the authority to prohibit the parent company’s subsidiary banks from engaging in unsafe or unsound practices in conducting their businesses.

- IMPACT OF MAJOR DEVELOPMENTS. On September 27, 2019, WFC’s board of directors announced the appointment of a new CEO after six months of uncertainty. Charles Scharf was formerly CEO of Visa Inc. and Bank of New York Mellon. Scharf has made the implementation of a risk and control framework appropriate for a bank of WFC’s size and complexity a top priority. Since 2019, regulators have terminated six consent orders.

- FINANCIAL PROFILE. WFC stated that with $1.9 trillion in total assets, the bank thinks it can meet its customers’ financial needs and deliver growth without increasing the bank’s balance sheet in the near term. Management is focused on reducing its exposure to riskier assets. We have also seen WFC be early versus its peers in tightening its credit risk discipline for new originations in commercial real estate during a period of increased competition.

- As of December 31, 2023, WFC’s Common Equity Tier 1 ratio was 11.4% in 2023 versus 10.6% in 2022, and 11.4% in 2021, and still above the regulatory minimum target of 8.9%. The bank’s tangible book value per share was $39.23 in 2023 versus $34.98 in 2022 and $36.35 in 2021. Its return on average tangible common equity (ROTCE) was 13.1% in 2023 compared to 9.3% in 2022 and 14.8% in 2021.

- WFC remains subject to an asset cap as part of the Fed’s consent order. Management must prioritize balance sheet usage more so than if it was not a limitation, which is a significant competitive constraint. Though WFC believes it’s making progress, there is still work to do. We think WFC may be able to return excess capital to shareholders through a combination of higher dividends and share buybacks. Management is assuming the asset cap will remain in place throughout 2024.

- In 2023, revenue jumped 11% Y/Y as results benefited from a 17% surge in net interest income. Noninterest income rose 3% as gains on trading activities and a rebound in investment banking fees outweighed weakness in deposit fees and mortgage banking. At the end of 2023, total loans outstanding were $937 billion, down 2% Y/Y, while total deposits were $1.36 trillion (-2%). In 2022, credit quality was excellent, with net charge-offs coming in at just 0.17%. However, net charge-offs jumped to 0.37% in 2023 as deterioration was identified in commercial real estate and credit card loans.

- WFC is a stable bank with multiple funding sources and credit risk management. In Q3 2024, the bank’s commercial real estate (CRE) loans represented $141 billion, or 16% of $910 billion of total loans, with office buildings at just $29 billion of

Discover more from TEN-NOJI

Subscribe to get the latest posts sent to your email.